Get the latest Swiss Re Institute sigma report by

Global economic growth has been stronger than anticipated so far this year, but a slowdown in the second half remains on the cards. Still-high inflation means today’s interest rate mantra is “higher for longer”, which has implications for the insurance sector also.

High interest rates sparked bank sector instabilities earlier this year but with their sound capital positions, insurers have not been shaken by the disruptions in the financial system. If anything, we expect the industry to demonstrate resilience over the next two years. We forecast that global insurance (non-life and life) premiums will grow by 1.1% in 2023 and 1.7% in 2024 in real terms, after contracting by 1.1% in 2022. And, reflecting the stirrings of market growth, we see premium volumes rising a new high this year, in nominal terms. Last year, the US, China and the UK ranked as the top 3 largest insurance markets in the world.

Non-life

In non-life, the main driver of the growth will be market hardening in commercial and now also personal lines, with insurers raising premium prices to offset inflation-induced rising claims costs. We see the motor segment returning to growth after three years of contraction, but a decline in health premiums due to the end of the pandemic support policies in the US could offset gains in other lines.

“With inflation pressures still persistent, hard market conditions in non‑life are set to continue as insurers offset elevated claims costs with higher premium prices. Once disinflation takes hold with prices decreasing, less expensive claims and greater returns from interest‑rate‑sensitive investments should further support industry profitability,” Jérôme Haegeli, Swiss Re’s Group Chief Economist said.

Life

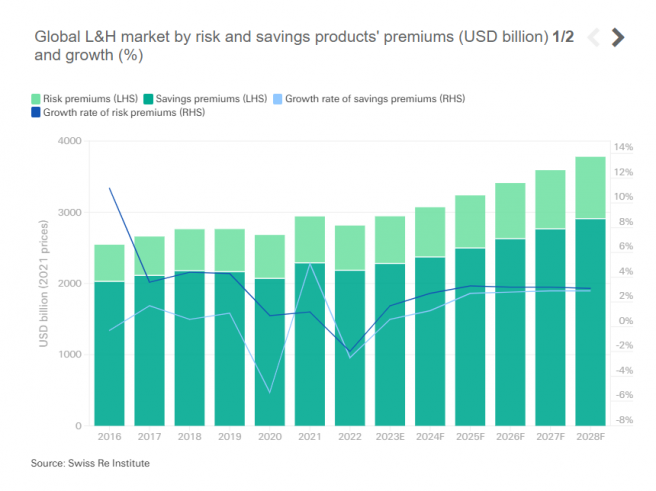

In life insurance, rising wages and interest rates in advanced markets are creating favourable growth and profitability tailwinds, including demand for annuities and pension risk transfer products. We also see new life risk pools in Hong Kong as a result of China’s reopening. Global savings products premiums should grow, driven by an estimated 4.3% gain in the emerging markets.

The profit outlook for life insurers is positive, based on four key drivers: improved investment returns, normalisation of COVID-19 related claims, a de-risking of pension and annuity premiums, and a stabilisation of earnings volatilities with implementation of the IFRS 17 accounting framework this year. On the downside, however, amidst the low growth and still-high inflation environment, we flag credit downgrades and lapses as two potential tail risks for sector earnings.

Get the sigma 3/2023 – World insurance report

New Sigma report: Natural catastrophes and inflation in 2022

Global economic and insurance market outlook 2023/24